The Library of Credit Portfolio Management

With the completion of Basel 2 financial institutions have established the prerequisite of modern credit risk management.

The Credit Risk Evaluator enables financial institutions to take the next step over the rating of single customers to an integrated risk and return management of the full bank portfolio.

Internal rating methods can create additional value for banks and financial institutions beyond a more economical equity allocation.

The Credit Risk Evaluator rests upon the data foundation laid by Basel 2 and links it to the modern credit portfolio models. It delivers and reports to the bank risk and return analyses on all portfolio levels from the single client or even the single deal over arbitrary aggregation levels to the full bank portfolio.

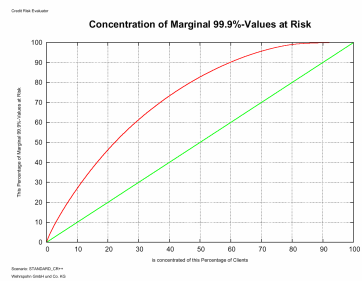

It creates the basis for the identification of the well diversified and the highly concentrated business and market areas up to the single client where the intended return on equity is reached or failed, respectively. From the results impulses can be derived for sales and management.

Design

The Credit Risk Evaluator is designed as an open library of credit portfolio models. It comprises today 7 models which can be applied in analyses by mouse-click:

Credit Metrics

The KMV model

A copula asset value model

Credit Risk+

Credit Risk++ - a generalization of Credit Risk+ for rating migrations, intersectoral correaltions and variable recovery models

A multi-period model that generalizes Credit Metrics and the KMV model.

A model that generalizes the copula asset value model to multiple periods.

All portfolio models can be combined with several recovery models to allow for a precise valuation of sub-portfolios and for the trading of credit risks.

Results

The Credit Risk Evaluator aims at an integrated view of risk and return. Under both aspects it delivers a number of key indicators on all levels of the analysis:

Value at risk, shortfall, standard deviation, expected loss

RAROC, economic value added (EVA), risk adjusted return, costs of risk, costs of equity

Technical aspects

The Credit Risk Evaluator is componente oriented in design. Data storage, business logic and control and reporting are technically fully separated from each other and can be distributed to different computers.

The performance is model dependent. It is for the single-period models between 3-7 minutes per 100,000 clients and 10,000 simulation runs on a standard pc. For the multi-period models the runtime slightly higher. In all cases the run times scales linearly in the number of clients and simulation runs.

Analyses can be done with manual intervention as batch-processes. Reports are automatically generated and archived at runtime.

Correlations and parametrization

Credit portfolio management often requires data that is not immediately at hand.

We aid you to determine correlations and other model parameters relating to your portfolio so that you can make full use of the potential of credit portfolio models.

Your advantages

Additional usage of the investments into Basel 2

Bank-wide portfolio management also in large institutions possible

State-of-the-art credit portfolio and recovery models at hand

Extendible for bank owned portfolio and recovery models

Simultaneous consideration of risks and returns

Highly automatized processing with minimum manual intervention

No comments:

Post a Comment