Privacy Policy for economicalvaluenewbasic.blogspot.com

If you require any more information or have any questions about our privacy policy, please feel free to contact us by email at indra.sakera@gmail.com.

At economicalvaluenewbasic.blogspot.com, the privacy of our visitors is of extreme importance to us. This privacy policy document outlines the types of personal information is received and collected by economicalvaluenewbasic.blogspot.com and how it is used.

Log Files

Like many other Web sites, economicalvaluenewbasic.blogspot.com makes use of log files. The information inside the log files includes internet protocol ( IP ) addresses, type of browser, Internet Service Provider ( ISP ), date/time stamp, referring/exit pages, and number of clicks to analyze trends, administer the site, track user’s movement around the site, and gather demographic information. IP addresses, and other such information are not linked to any information that is personally identifiable.

Cookies and Web Beacons

economicalvaluenewbasic.blogspot.com does use cookies to store information about visitors preferences, record user-specific information on which pages the user access or visit, customize Web page content based on visitors browser type or other information that the visitor sends via their browser.

DoubleClick DART Cookie

.:: Google, as a third party vendor, uses cookies to serve ads on economicalvaluenewbasic.blogspot.com.

.:: Google's use of the DART cookie enables it to serve ads to users based on their visit to economicvalueaddbasic.blogspot.com and other sites on the Internet.

.:: Users may opt out of the use of the DART cookie by visiting the Google ad and content network privacy policy at the following URL - http://www.google.com/privacy_ads.html

Some of our advertising partners may use cookies and web beacons on our site. Our advertising partners include ....

Google Adsense

These third-party ad servers or ad networks use technology to the advertisements and links that appear on economicalvaluenewbasic.blogspot.com send directly to your browsers. They automatically receive your IP address when this occurs. Other technologies ( such as cookies, JavaScript, or Web Beacons ) may also be used by the third-party ad networks to measure the effectiveness of their advertisements and / or to personalize the advertising content that you see.

economicalvaluenewbasic.blogspot.com has no access to or control over these cookies that are used by third-party advertisers.

You should consult the respective privacy policies of these third-party ad servers for more detailed information on their practices as well as for instructions about how to opt-out of certain practices. economicalvaluenewbasic.blogspot.com's privacy policy does not apply to, and we cannot control the activities of, such other advertisers or web sites.

If you wish to disable cookies, you may do so through your individual browser options. More detailed information about cookie management with specific web browsers can be found at the browsers' respective websites.

Sunday, 12 December 2010

Thursday, 19 August 2010

International Growth Highlights Wal-Mart's 2Q

We own WalMart (WMT) because it adopted value-based management a few years back. It made return on invested capital its overarching objective. The result was a change in strategy. Instead of driving sales growth by investing vast amounts in new stores in already saturated markets, WMT cut back on domestic capital spending and drove US productivity.

It also exited markets like Germany where expected returns were below its cost of capital. The growth would come from the fast growing emerging markets of China and South America. Those are the places that very profitable growth continues as was reported in today's earnings release. From Morningstar $$:

Wal-Mart's competitive advantages and everyday low pricing strategy will stand under any operating environment. Moreover, as Wal-Mart gains traction in several high-growth markets such as Mexico, China, and Brazil, the international segment will become an increasingly critical component of our valuation assumptions. Trading at less than 13 times our forward earnings estimate and an enterprise value/EBITDA under 7 times, Wal-Mart shares look attractive.

Using excess cash flow to reduce shares outstanding has added about 2% to EPS growth since 2005. With recession over in its business, WMT has stepped up buying shares so the increased ownership for existing shareholders will add about 4% to EPS growth.

Intrinsic Value

In the graph below we see WalMart's intrinsic value (red line) as measured by afgview.com's default model matched up against share price (the blue columns). You can see the increasing gap between a rising intrinsic value and falling or at best stagnant stock price. These are widening gaps give us our margin of safety. We can see that after the recession '08-09, the gap is beginning to widen again.

Wealth Creators vs. Wealth Destroyers: Best Buy Co., Inc. (NYSE:BBY) vs. Circuit City

Analysts tend to miss the forest for the trees. In retail they are obsessed with the business model drivers like sales per square foot, same store sales or gross margin. Certainly, these metrics are important for understanding the dynamics of a retail business - but to what end?

The bottom line is whether a business model and management team create value per share - that's the single minded objective function for any for profit business. It's the only one that allows for principled trade-offs between competing subordinate goals. The answer is always the combination of drivers that will yield the most value over time.

AFGview.com's economic margin framework accomplishes this simple but overlooked goal. See below for an example comparison of Best Buy to Circuit City.

On ValueExpectations.com we always talk about a company’s true economic profitability (Economic Margin) to see through some of the distortions caused by traditional accounting practices and better understand what a company is truly earning above or below its cost of capital# We have shown through numerous examples that a company’s Economic Margin (EM) level is highly correlated with its market performance and an increase in margins typically leads to market out performance, where a decline in margins leads to market under performance# The example below shows both ends of the spectrum, one company that generates positive EMs and is able to grow its business while maintaining its profitability while the other company was unable to earn its cost of capital and consistently deteriorated its EMs.

It is no surprise based on economic profitability that Best Buy Co., Inc. is still doing quite well in the retail arena and has done a good job of growing its business while maintaining its profitability. The market tends to reward companies that grow profitable businesses and relative to the market BBY has consistently outperformed the S&P 500. Circuit City on the other hand deteriorated its EMs over time and eventually was unable to survive.

The Economic Margin (EM) Framework was developed to evaluate corporate performance from an economic cash flow perspective and is an alternative to accounting-based valuation metrics. EM measures the return a company earns above or below its cost of capital and provides a more complete view of a company’s underlying economic strength.

EM is meant to serves two purposes: Create a measure of a company’s economic profitability; that is, did this company generate cash flow in excess of the costs of its capital invested in its operations, or did the company destroy wealth? Once we have solved for this, we can then use this EM as a function in our valuation model.

EM is calculated by dividing a company’s Operating Cash Flow minus Capital Charge by their Invested Capital.

It is not uncommon for companies to grow EPS while having declining or negative EM’s. This occurs when the cost for the investment required to yield the EPS (cost of capital) is more than the cash flow generated from the investment. From an economic perspective, this is growing EPS at the expense of the economics of the business.

Unlike traditional measures, EM considers the “profitability” of EPS growth, eliminates accounting distortions, and are comparable across time and industry. By analyzing a company’s EMs through time, investors gain a more accurate account of levels and changes in a company’s current profitability and value.

Structure and Development of the Economy

With its strategic location at the doorway to the Mainland and on the international time zone that bridges the time gap between Asia and Europe, the HKSAR has been serving as a global centre for trade, finance, business and communications. Hong Kong is now ranked the 11th largest trading entity in the world. It operates the busiest container port in the world in terms of throughput, as well as one of the busiest airports in terms of number of international passengers and volume of international cargo handled. In addition, it is the world's 12th largest banking centre in terms of external banking transactions, and the seventh largest foreign exchange market in terms of turnover. Its stock market is Asia's second largest in terms of market capitalisation.

Hong Kong is characterised by a high degree of internationalisation, business-friendly environment, rule of law, free trade and free flow of information, open and fair competition, well-established and comprehensive financial network, superb transport and communications infrastructure, sophisticated support services, and a skilled and well educated workforce complemented by a pool of effective and enterprising entrepreneurs. Added to these are the substantial amount of fiscal reserves and foreign exchange reserves, a fully convertible and stable currency, and a simple tax system with a low tax rate. On these virtues, Hong Kong is widely regarded as amongst the freest and most competitive economies in the world. The US Heritage Foundation ranks Hong Kong as the world's freest economy for the 10th year in a row in 2004. The Cato Institute of the United States, in conjunction with the Fraser Institute of Canada and other research bodies around the world, also consistently ranks Hong Kong as the freest economy in the world.

Over the past two decades, the Hong Kong economy has more than doubled in size, with GDP growing at an average annual rate of 5.0 per cent in real terms. This outpaces considerably the growth of the world economy and the Organisation for Economic Cooperation and Development (OECD) economies. Over the same period, Hong Kong's per capita GDP doubled at constant price level, giving an average annual growth rate of 3.7 per cent in real terms. At US$23,300 in 2003, this per capita GDP was amongst the highest in Asia, next only to Japan (Chart 1).

In line with increased external orientation of the Hong Kong economy, trade in goods expanded by eight times and trade in services by almost three times in real terms over the past two decades. In 2003, the total value of visible trade (comprising re-exports, domestic exports and imports of goods) reached $3,543 billion, corresponding to 287 per cent of GDP. This was distinctly larger than the ratios of 156 per cent in 1983 and 230 per cent in 1993. If the value of exports and imports of services is also taken into account, the ratio is even greater, at 331 per cent in 2003, as compared to 192 per cent in 1983 and 267 per cent in 1993.

Chart 1

Gross Domestic Product

(year-on-year rate of change in real terms)

Over the past two decades, the Hong Kong economy grew at an average annual rate of 5.0 per cent in real terms, outpacing the corresponding growth rate of 2.8 per cent for OECD economies as a whole. In 2003, the economy still attained a 3.3 per cent growth in real terms, despite the impact of SARS.

As another indication of the high degree of external orientation, the stock of inward direct investment in Hong Kong amounted to $2,622 billion in market value at end-2002, equivalent to 208 per cent of GDP. Hong Kong is the second most favoured destination for inward direct investment in Asia, next only to the Mainland. The corresponding figures for the stock of outward direct investment in Hong Kong were likewise substantial, at $2,413 billion and 192 per cent of GDP, much larger than those for many other economies in Asia. As a major financial centre in the region with huge cross-territory fund flows, Hong Kong's external financial assets and liabilities were also substantial, at $8,033 billion and $5,355 billion respectively at end-2002. The corresponding ratios to GDP in that year were 638 per cent and 425 per cent. Reflecting Hong Kong's sound international investment position, net external financial assets amounted to $2,677 billion at end-2002, equivalent to 213 per cent of GDP. As to gross external debt, which is the sum of the non-equity liability components in international investment, it stood at $2,803 billion at end-2003, equivalent to 227 per cent of GDP. Yet a major proportion of it arose from normal operations of the banking sector, and the Government incurred no external debt at all.

The Gross National Product (GNP), comprising GDP and net external factor income flows, stood at $1,269 billion in 2003. This was higher than the corresponding GDP by 2.8 per cent, owing to sustained net inflow of external factor income. In gross terms, inflows and outflows of external factor income remained substantial in 2003, at $329 billion and $294 billion respectively, equivalent to 27 per cent and 24 per cent of GDP. This was related to the huge volume of both inward and outward investment in Hong Kong.

Contributions of the Various Economic Sectors

Primary production (including agriculture, fisheries, mining and quarrying) is insignificant in Hong Kong, in terms of both value added contribution to GDP and share in total employment. This reflects the predominantly urbanised nature of the economy.

Secondary production (comprising manufacturing, construction, and supply of electricity, gas and water), which constituted a significant contributor to GDP up to the early 1980s, has diminished in relative importance since then. Within this broad sector, the value added contribution from manufacturing shrank from 21 per cent in 1982 to 14 per cent in 1992 and distinctly more to only 5 per cent in 2002, consequential to ongoing relocation of the more labour-intensive production processes to the Mainland. For the construction sector, its contribution to GDP edged lower from 7 per cent in 1982 to 5 per cent in 1992, and further to 4 per cent in 2002. As to supply of electricity, gas and water, the corresponding share held relatively stable, at around 2-3 per cent over the past two decades.

The open door policy and economic reform in the Mainland have not only provided an enormous production hinterland and market outlet for Hong Kong's manufacturers, but have also created abundant business opportunities for a wide range of service activities. These activities include specifically freight and passenger transport, travel and tourism, telecommunications, banking, insurance, real estate, and professional services such as financial, legal, accounting and consultancy services. In consequence, the Hong Kong economy has become increasingly service-oriented since the 1980s.

Reflecting this, the share of the tertiary services sector (comprising the wholesale, retail and import/export trades, restaurants and hotels; transport, storage and communications; financing, insurance, real estate and business services; community, social and personal services; and ownership of premises) in GDP went up visibly, from 69 per cent in 1982 to 79 per cent in 1992 and further to 88 per cent in 2002 (Chart 2).

The profound change in the economic structure was also borne out by a broadly similar shift in the sectoral composition of employment. Over the past two decades, the share of the services sector in total employment followed a continuous uptrend, rising distinctly from 52 per cent in 1983 to 73 per cent in 1993 and further to 85 per cent in the first three quarters of 2003. On the other hand, the corresponding share for the manufacturing sector kept on shrinking, from 38 per cent in 1983 to 18 per cent in 1993 and further to only 5 per cent in the first three quarters of 2003 (Chart 3).

The services sector has not only flourished but also diversified in types of activities, concomitant with the structural transformation of the economy. Trade-related and tourism-related services, community, social and personal services, and finance and business services such as banking, insurance, real estate and a host of related professional services, have all grown distinctly over the past two decades. Strong expansion was also observed in information technology in the more recent years, especially those pertaining to telecommunications services and Internet applications, in line with the shift in economic structure more towards knowledge-based activities.

Chart 2

Gross Domestic Product by broad economic sector

Along with a profound shift in economic structure, the share of the tertiary services sector in GDP continued to increase, while the share of the secondary sector dwindled further over the past two decades.

Chart 3

Employment by broad economic sector

Consequential to the ongoing relocation of the less skill-intensive and lower value added manufacturing processes to the Mainland, as well as the strong growth in service activities in Hong Kong, the tertiary services sector has expanded markedly and has overtaken the secondary sector to become the largest employer in the economy since 1981.

* Average of Q1 to Q3 2003.

On trade in services, exports and imports of services both grew by an annual average of 7 per cent in real terms over the past two decades. In 2002, civil aviation, travel and tourism, trade-related services, and various financial and banking services were the largest components of trade in services. Within exports of services, offshore trading and merchandising services have overtaken transportation as the most important component in 2002, accounting for 35 per cent of the total value in that year. For transportation, the corresponding share was 30 per cent. This was followed by travel and tourism (with a share of 17 per cent), and financial and banking services (6 per cent). As to imports of services, travel and tourism remained the largest component, accounting for 50 per cent of the total value in 2002. Transportation was in the second place (with a share of 26 per cent), followed by offshore trading and merchandising services (7 per cent), and financial and banking services (3 per cent).

Net output or value added of the services sector as a whole rose visibly, by an annual average of 6 per cent in value terms between 1992 and 2002. Amongst the major constituent sectors, net output of community, social and personal services had the fastest growth (at an average annual rate of 9 per cent). This was followed by transport, storage and communications (6 per cent); the wholesale, retail and import/export trades, restaurants and hotels (5 per cent); and financing, insurance, real estate and business services (4 per cent).

In terms of value added contribution to GDP, the wholesale, retail and import/export trades, restaurants and hotels continued to be the largest in 2002, with a share of 27 per cent. This was followed by community, social and personal services (22 per cent), financing, insurance, real estate and business services (22 per cent), and transport, storage and communications (11 per cent) (Chart 4).

Chart 4

Gross Domestic Product by major service sector

Over the past two decades, community, social and personal services had a more distinct increase in net output than other major service sectors. Yet ranked in terms of value added contribution to GDP, the wholesale, retail and import/export trades, restaurants and hotels remained the largest service sector in 2002.

In terms of employment, the wholesale, retail and import/export trades, restaurants and hotels was again the largest sector, accounting for 31 per cent of the total employment in the first three quarters of 2003. This was followed by community, social and personal services (with a share of 28 per cent), financing, insurance, real estate and business services (15 per cent), and transport, storage and communications (11 per cent) (Chart 5).

Chart 5

Employment by major service sector

Over the past two decades, financing, insurance, real estate and business services showed the fastest employment growth. But in terms of employment size, the wholesale, retail and import/export trades, restaurants and hotels continued to be the largest employer in the economy in 2003. * Average of Q1 to Q3 2003. The Manufacturing Sector Manufacturing firms in Hong Kong are renowned for their versatility and flexibility in coping with changing demand conditions in the overseas markets. Moreover, through increased outward processing arrangements in the Mainland, Hong Kong's productive capacity has effectively been expanded by multiples, which has helped uphold the price competitiveness of its products. Besides relocating the more labour-intensive production processes to the Mainland, Hong Kong's manufacturers have also been striving hard to diversify their products and markets, in face of the challenges from globalisation of trade and keen competition from other export producers. Concurrently, productive efficiency and product quality have been continuously upgraded by incorporating more advanced skills and technology. Within the local manufacturing sector, textiles and clothing remain the most important industries, notwithstanding continued decline in their relative significance over the years. Other major industries include machinery and equipment, electronics, printing and publishing, food processing and metal products. Generally speaking, those manufacturing operations still remaining in Hong Kong are more knowledge-based with a higher value added and a greater technology content. Between 1993 and 2003, labour productivity in the local manufacturing sector, as measured by the ratio of the industrial production index to the manufacturing employment index, rose visibly, by an annual average of around 6 per cent. In 2003, the United States and the Mainland were the two largest markets for Hong Kong's domestic exports, accounting for 32 per cent and 30 per cent respectively of the total. Other major markets included the United Kingdom (6 per cent), Germany (4 per cent), Taiwan (3 per cent), Japan (2 per cent), and the Netherlands (2 per cent). In the more recent years, new markets have been developed for Hong Kong's exports, including markets in the Middle East, Eastern Europe, Latin America and Africa. Increasing Economic Links between the HKSAR and the Mainland Since the Mainland adopted its economic reform and open door policy in 1978, economic links between Hong Kong and the Mainland have gone from strength to strength. This has brought substantial economic benefits to both places. Visible trade between Hong Kong and the Mainland has expanded rapidly since 1978, at an average annual rate of 22 per cent in value terms. But the pace of growth moderated in the more recent years, to an annual average of 8 per cent during 1993-2003, partly due to increased direct shipment of goods into and out of the Mainland upon enhancement of port facilities and simplification of customs procedures there. The Mainland remained Hong Kong's largest trading partner in 2003, accounting for 43 per cent of the total trade value in Hong Kong. The bulk (specifically, 91 per cent) of Hong Kong's re-export trade was related to the Mainland, making it the largest market for as well as the largest source of Hong Kong's re-exports. Reciprocally, Hong Kong was the Mainland's third largest trading partner in 2003 (after Japan and the United States), accounting for 10 per cent of the Mainland's total trade value (Chart 6). In the more recent years, there has been an increasing shift in the mode of Hong Kong-Mainland trade from re-exports to offshore trade. Between 1990 and 1995, Hong Kong's exports of trade-related services grew at an annual average rate of 5 per cent in real terms, much slower than the growth in re-exports involving the Mainland, at an annual average rate of 22 per cent. The growth pattern was reversed during 1995 to 2003, when exports of trade-related services surged at an average annual rate of 15 per cent in real terms, outpacing the growth in re-exports involving the Mainland, at an average annual rate of 7 per cent. Over the past two decades, there has also been a sharp increase in people, service and investment flows between Hong Kong and the Mainland. Hong Kong is a major service centre for the Mainland generally and South China in particular, providing a wide array of financial and other business support services like banking and finance, insurance, transport, accounting and sales promotion. Hong Kong is also a principal gateway to the Mainland for business and tourism. Between 1993 and 2003, the number of trips made by Hong Kong residents to the Mainland grew at an average annual rate of 9 per cent to 53 million trips, and the number of trips made by foreign visitors to the Mainland through Hong Kong at an average annual rate of 4 per cent to 2.7 million trips. Yet, mainly due to the outbreak of SARS in the region in the first half of the year, these two particular types of trips decreased by 6 per cent and 21 per cent respectively in 2003. Chart 6 Visible trade between Hong Kong and the Mainland

|

Economic Value Added (EVA) - How to Calculate Economic Viability of a Corporation

i) Economic Value Added is used as a performance evaluation tool of higher level managers, directors, VPs and CEOs of a corporation because the performance of the organization depends on the human resources deployed.

ii) Economic Value Added is used at sub-division level & entire organizational level of the business, unlike other methods such as Market Value Added that only focuses on the big picture of a corporation.

iii) Economic Value Added factors in to performance evaluation that the operating net income of a corporation must cover both operating costs of the organization as well as the capital costs (opportunity cost of capital). This is unlike other accounting methods such as EBIT or EBITDA or Net Income that look at total revenues generated by the business minus total expenses as a performance evaluation tool.

Economic Contributions - 2008 Performance

The economic contribution we make to society is much more than the financial profits we derive. Our contribution includes the value that flows from the broader contributions of our operations, such as payments to our employees and suppliers and disbursements to governments, including taxes and royalties.

The following provides an outline of:

Our Financial Performance

The broader economic contributions we make to society through our Economic Value Generated and Distributed.

Economic Value Generated and Distributed

Economic value generated and distributed, as defined in the Global Reporting Initiative (2006 version), provides an economic profile or context of the reporting organisation and a useful picture of direct monetary value added to regional economies.

Economic value generated and distributed, as defined in the Global Reporting Initiative (2006 version), provides an economic profile or context of the reporting organisation and a useful picture of direct monetary value added to regional economies.

The measure includes revenues, operating costs, employee compensation, donations and other community investments, retained earnings, and payments to capital providers and to governments. The breakdown of this amount by category is presented below and shows expenditure by region to help to quantify the regional economic contributions of the Company. Refer table below.

Extractive Industries Transparency Initiative

Extractive Industries Transparency Initiative

The Extractive Industries Transparency Initiative (EITI) is gaining momentum as an international initiative bringing together companies, investors, governments, international financial institutions and civil society to improve disclosure and tracking of revenues in developing countries.

We remain supportive of EITI but note that implementation in the countries where we operate has not yet progressed to the point where an appropriate framework for reporting is in place. We remain committed to constructive engagement with our host governments as they seek to progress implementation.

The following provides an outline of:

Our Financial Performance

The broader economic contributions we make to society through our Economic Value Generated and Distributed.

Economic Value Generated and Distributed

The measure includes revenues, operating costs, employee compensation, donations and other community investments, retained earnings, and payments to capital providers and to governments. The breakdown of this amount by category is presented below and shows expenditure by region to help to quantify the regional economic contributions of the Company. Refer table below.

The Extractive Industries Transparency Initiative (EITI) is gaining momentum as an international initiative bringing together companies, investors, governments, international financial institutions and civil society to improve disclosure and tracking of revenues in developing countries.

We remain supportive of EITI but note that implementation in the countries where we operate has not yet progressed to the point where an appropriate framework for reporting is in place. We remain committed to constructive engagement with our host governments as they seek to progress implementation.

Value-Added Production

Resource-dependent communities have historically captured little of the enormous wealth that has flowed through them. They have simply extracted raw materials, creating relatively few jobs while remaining at the mercy of external market forces and owners. Most of the economic value has been generated elsewhere.

In contrast, local economies are able to turn raw resources, both local and imported, into a wide range of products and services. Such economies can effectively harness skilled labor and specialized equipment to add many layers of value to every tree, fish, mineral, or crop. They provide more economic activity — and therefore more jobs — per unit of resource, decreasing pressure on nature and enhancing social equity.

Timbre Tonewood, based on Vancouver Island, provides an excellent example of value-added production. The company, which makes spruce and cedar guitar tops, carefully evaluates every piece of wood that comes through its mill. Based on their appearance, the dried planks are sorted into nine different grades, ranging from the low-end tops, which will probably be painted, to the very best — distinguished by their creamy color, their even ring pattern, and rays running across the grain.

Timbre Tonewood's by-products feed the local economy as well. A local box-maker uses some of the pieces that are too small or irregular to be made into guitar tops for smoked salmon cases. Using waste as resource, another local entrepreneur blends the sawdust from the operation with shrimp shells to make compost.

Value-added products have also been developed from timber (including flooring, lumber, furniture, crafts, etc.), seafood (premium products created through careful processing and decreasing time to market), agriculture (specialty products like jams, sauces, packaged foods), and many other sources.

Add value locally by careful application of appropriate skills and equipment, creating additional jobs without increasing the strain on ecosystems. This helps maintain a stable and diverse local economy

Finance and Insurance Industries Led Slowdown in 2007

Revised Statistics of Gross Domestic Product by Industry

A sharp slowdown in finance and insurance, a further contraction in construction, and a deceleration in durable-goods manufacturing were the leading contributors to the economic slowdown in 2007, according to revised statistics of real gross domestic product (GDP) by industry from the Bureau of Economic Analysis.

Finance and insurance industries” value added–a measure of an industry’s contribution to GDP’slowed to 0.1 percent in 2007 after increasing 6.3 percent in 2006.

Construction’s value added continued to decline, dropping 11.2 percent in 2007 after falling 4.1 percent in 2006, reflecting the further decline in residential building.

Durable-goods manufacturing value added slowed to 4.8 percent from an 8.1 percent increase. Decelerations were reported in 8 of 11 durable-goods manufacturing industries.

Prices:

Prices:

Slower growth in the value added price indexes for construction and utilities industries contributed most to the slowdown in the overall GDP price index in 2007. The value added price index, which measures changes in an industry’s labor and capital input prices including its profit margin, accelerated sharply in the agriculture, forestry, fishing, and hunting industry group.

Other highlights:

Other highlights:

Private services-producing industries accounted for most of the 2.0 percent growth in real GDP in 2007. Professional and business services and real estate and rental and leasing were the largest contributors to overall economic growth.

Private goods-producing industries subtracted from GDP growth in 2007 for the first time since 2001, reflecting the 11.2 percent drop in construction value added.

Information-communication-technology-producing (ICT) industries” value added remained strong in 2007, increasing 13.0 percent. These industries account for 4 percent of GDP, but accounted for over 20 percent of real GDP growth in 2007.

A sharp slowdown in finance and insurance, a further contraction in construction, and a deceleration in durable-goods manufacturing were the leading contributors to the economic slowdown in 2007, according to revised statistics of real gross domestic product (GDP) by industry from the Bureau of Economic Analysis.

Finance and insurance industries” value added–a measure of an industry’s contribution to GDP’slowed to 0.1 percent in 2007 after increasing 6.3 percent in 2006.

Construction’s value added continued to decline, dropping 11.2 percent in 2007 after falling 4.1 percent in 2006, reflecting the further decline in residential building.

Durable-goods manufacturing value added slowed to 4.8 percent from an 8.1 percent increase. Decelerations were reported in 8 of 11 durable-goods manufacturing industries.

Slower growth in the value added price indexes for construction and utilities industries contributed most to the slowdown in the overall GDP price index in 2007. The value added price index, which measures changes in an industry’s labor and capital input prices including its profit margin, accelerated sharply in the agriculture, forestry, fishing, and hunting industry group.

Private services-producing industries accounted for most of the 2.0 percent growth in real GDP in 2007. Professional and business services and real estate and rental and leasing were the largest contributors to overall economic growth.

Private goods-producing industries subtracted from GDP growth in 2007 for the first time since 2001, reflecting the 11.2 percent drop in construction value added.

Information-communication-technology-producing (ICT) industries” value added remained strong in 2007, increasing 13.0 percent. These industries account for 4 percent of GDP, but accounted for over 20 percent of real GDP growth in 2007.

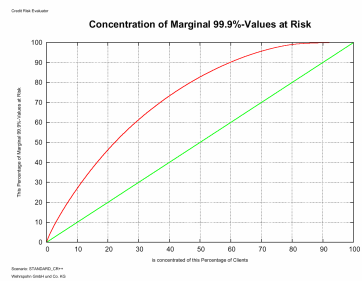

Credit Risk Evaluator

The Library of Credit Portfolio Management

With the completion of Basel 2 financial institutions have established the prerequisite of modern credit risk management.

The Credit Risk Evaluator enables financial institutions to take the next step over the rating of single customers to an integrated risk and return management of the full bank portfolio.

Internal rating methods can create additional value for banks and financial institutions beyond a more economical equity allocation.

The Credit Risk Evaluator rests upon the data foundation laid by Basel 2 and links it to the modern credit portfolio models. It delivers and reports to the bank risk and return analyses on all portfolio levels from the single client or even the single deal over arbitrary aggregation levels to the full bank portfolio.

It creates the basis for the identification of the well diversified and the highly concentrated business and market areas up to the single client where the intended return on equity is reached or failed, respectively. From the results impulses can be derived for sales and management.

Design

The Credit Risk Evaluator is designed as an open library of credit portfolio models. It comprises today 7 models which can be applied in analyses by mouse-click:

Credit Metrics

The KMV model

A copula asset value model

Credit Risk+

Credit Risk++ - a generalization of Credit Risk+ for rating migrations, intersectoral correaltions and variable recovery models

A multi-period model that generalizes Credit Metrics and the KMV model.

A model that generalizes the copula asset value model to multiple periods.

All portfolio models can be combined with several recovery models to allow for a precise valuation of sub-portfolios and for the trading of credit risks.

Results

The Credit Risk Evaluator aims at an integrated view of risk and return. Under both aspects it delivers a number of key indicators on all levels of the analysis:

Value at risk, shortfall, standard deviation, expected loss

RAROC, economic value added (EVA), risk adjusted return, costs of risk, costs of equity

Technical aspects

The Credit Risk Evaluator is componente oriented in design. Data storage, business logic and control and reporting are technically fully separated from each other and can be distributed to different computers.

The performance is model dependent. It is for the single-period models between 3-7 minutes per 100,000 clients and 10,000 simulation runs on a standard pc. For the multi-period models the runtime slightly higher. In all cases the run times scales linearly in the number of clients and simulation runs.

Analyses can be done with manual intervention as batch-processes. Reports are automatically generated and archived at runtime.

Correlations and parametrization

Credit portfolio management often requires data that is not immediately at hand.

We aid you to determine correlations and other model parameters relating to your portfolio so that you can make full use of the potential of credit portfolio models.

Your advantages

Additional usage of the investments into Basel 2

Bank-wide portfolio management also in large institutions possible

State-of-the-art credit portfolio and recovery models at hand

Extendible for bank owned portfolio and recovery models

Simultaneous consideration of risks and returns

Highly automatized processing with minimum manual intervention

A new way to value the market

(Fortune Magazine) -- Are stocks cheap yet? That slippery, eternal question is worth a look right now because a remarkable new set of data has just become available, allowing us to analyze the market in ways we never could before. I wish I could tell you that this new trove of numbers reveals that stocks are a screaming buy. It doesn't. But it does suggest that, amid all the recent tumult, just maybe the market is being rational.

The new data are derived from the most fundamental, capital-based way of analyzing a company's finances and value. How much capital is a company using? What is its return on capital? How much does the capital cost? Those questions hold the key to corporate performance, but finding the answers in most financial statements isn't easy, and many executives don't know the answers themselves. The Stern Stewart consulting firm began popularizing these concepts more than 15 years ago with the term EVA (economic value added), and the new data come from EVA Dimensions, a firm that is now the source of Stern Stewart's EVA data.

EVA-based analysis has proven extremely valuable in analyzing individual companies. I almost never make calls on specific stocks, but in late 1999 the EVA analysis of AOL was so compelling that I wrote a column declaring flatly that the stock price could not possibly be justified. That column was published on Jan. 10, 2000, right near the overall market peak (and the very day that AOL announced it was using its insanely overvalued stock to buy my employer, Time Warner (TWX, Fortune 500) - but that's another story). I also used EVA analysis to write last summer that Google (GOOGLE) was overpriced at $540; that call looked wrong for a while, though as I write this the stock is at $501.

One thing you couldn't do with EVA analysis was use it to value the whole market. Compiling the data for a significant number of companies used to take months. But now, through the miracles of our networked world, EVA Dimensions can compile it every day for 2,669 companies in the Russell 3000 (those for which at least two years of data are available). This is essentially the U.S. stock market. So: Is it worth what it costs?

Look first at how well the companies are doing at their most basic task, which is earning a return on their capital that's greater than the total cost of that capital. Turns out they've been doing very well. The dollar difference between their return on capital and cost of capital (their EVA) was $375 billion over the past four quarters. It was only half that much in 2005, and in 2004 it was negative, which isn't surprising. Over time, for the broader market, EVA should be more or less zero since competition is always forcing high returns down toward the cost of capital, while companies that can't meet their capital cost will eventually go under. So America's publicly traded companies did great last year; in fact, with economic growth strong through the third quarter, it's safe to say that they were at or near the top of the business cycle.

Next question: How are they being valued? On a recent day when the Dow closed at 12,265, the 2,669 Russell 3000 companies had a total enterprise value of $29.8 trillion (equity plus debt). To judge whether that's a lot or a little, consider that over the past four quarters these companies produced after-tax operating profits of about $1.8 trillion. Even if we assume that earnings will only match, not exceed, that level in future years, then the companies' aggregate market value today would still be $22.5 trillion (note to finance wonks: that's their profits capitalized at their capital cost of about 8.1%), which is about 75% of their actual market value.

So now we reach the central question. About 25% of the current market value of these companies is based on expectations of future profits above and beyond the profits they earned last year, at the top of the business cycle. Does that seem reasonable? Actually, it just might. The math gets a bit tedious, but you can assume no profit growth for the next several years and very modest growth thereafter, and the valuation still looks okay.

The new data are derived from the most fundamental, capital-based way of analyzing a company's finances and value. How much capital is a company using? What is its return on capital? How much does the capital cost? Those questions hold the key to corporate performance, but finding the answers in most financial statements isn't easy, and many executives don't know the answers themselves. The Stern Stewart consulting firm began popularizing these concepts more than 15 years ago with the term EVA (economic value added), and the new data come from EVA Dimensions, a firm that is now the source of Stern Stewart's EVA data.

EVA-based analysis has proven extremely valuable in analyzing individual companies. I almost never make calls on specific stocks, but in late 1999 the EVA analysis of AOL was so compelling that I wrote a column declaring flatly that the stock price could not possibly be justified. That column was published on Jan. 10, 2000, right near the overall market peak (and the very day that AOL announced it was using its insanely overvalued stock to buy my employer, Time Warner (TWX, Fortune 500) - but that's another story). I also used EVA analysis to write last summer that Google (GOOGLE) was overpriced at $540; that call looked wrong for a while, though as I write this the stock is at $501.

One thing you couldn't do with EVA analysis was use it to value the whole market. Compiling the data for a significant number of companies used to take months. But now, through the miracles of our networked world, EVA Dimensions can compile it every day for 2,669 companies in the Russell 3000 (those for which at least two years of data are available). This is essentially the U.S. stock market. So: Is it worth what it costs?

Look first at how well the companies are doing at their most basic task, which is earning a return on their capital that's greater than the total cost of that capital. Turns out they've been doing very well. The dollar difference between their return on capital and cost of capital (their EVA) was $375 billion over the past four quarters. It was only half that much in 2005, and in 2004 it was negative, which isn't surprising. Over time, for the broader market, EVA should be more or less zero since competition is always forcing high returns down toward the cost of capital, while companies that can't meet their capital cost will eventually go under. So America's publicly traded companies did great last year; in fact, with economic growth strong through the third quarter, it's safe to say that they were at or near the top of the business cycle.

Next question: How are they being valued? On a recent day when the Dow closed at 12,265, the 2,669 Russell 3000 companies had a total enterprise value of $29.8 trillion (equity plus debt). To judge whether that's a lot or a little, consider that over the past four quarters these companies produced after-tax operating profits of about $1.8 trillion. Even if we assume that earnings will only match, not exceed, that level in future years, then the companies' aggregate market value today would still be $22.5 trillion (note to finance wonks: that's their profits capitalized at their capital cost of about 8.1%), which is about 75% of their actual market value.

So now we reach the central question. About 25% of the current market value of these companies is based on expectations of future profits above and beyond the profits they earned last year, at the top of the business cycle. Does that seem reasonable? Actually, it just might. The math gets a bit tedious, but you can assume no profit growth for the next several years and very modest growth thereafter, and the valuation still looks okay.

Canada’s natural resource exports

Introduction

The recent boom in commodity markets has returned the spotlight to Canada’s natural resources, most of which are exported. The importance of resources to our overall exports is often discussed, with a figure of 40% commonly cited.1 This share has risen to 50% of gross exports thanks to the commodity boom of the last two years. But subtracting out the higher import content of manufactured exports raises the share of resources to over 60%. This puts Canada in a unique class of major industrial nations, alongside nations such as Norway and Australia, where resource exports dominate. They are the polar opposite of Japan, which imports most of its resources and exports almost none.

These estimates are usually arrived at by calculating the share of agricultural, energy, forestry and industrial materials in gross exports. But this method does not account for the difference between gross and value-added exports. As noted in our previous studies2, firms shifted to using markedly more imports in their production process in the 1990s. This phenomenon was most pronounced for autos and machinery and equipment, which import nearly half their inputs. This reflects the greater use by manufacturers of standardized parts, often made just across the US border or sometimes overseas.

As a result, much of the growth of gross exports in the last decade reflected the increasing use of imported components, not higher value-added exports. Value-added exports, which include only inputs purchased in Canada, are the key determinant of domestic output and jobs.

Conversely, many of our leading resource products have a largely extractive production process that requires few imports apart from machinery and equipment.

The implication is clear: the importance of industries such as autos that make liberal use of imports is overstated by gross exports, while industries that import less actually have a larger role than gross exports suggest, notably natural resources. This paper looks at the true role of resources in value-added exports in Canada.

The main motivation behind the growing use of imports was the relentless drive by firms to search out the lowest possible cost for inputs. As well, the rise in the Canadian dollar in the early 1990s lowered the cost of imports, giving firms an added incentive to purchase abroad. But the steady drop in the dollar from 1997 to 2003 took away much of this latter incentive, and the use of imported inputs leveled off in recent years. The recent recovery may encourage firms to buy more imported inputs.

Sectoral share of exports

In terms of the share of gross exports, autos and machinery and equipment led with about 22% in 2004. Despite their recent surge, the four resource sectors followed, led by industrial goods3 (notably metal products) and energy at 19% and 17% respectively. Forestry and agricultural products were next at 9% and 7%. Together, these four resource sectors accounted for just under half of all exports. Consumer goods trail at 4%, although they have grown the fastest, doubling their share since 1989, led by pharmaceuticals.

Figure 1

However, this ranking changes radically when the import content of exports is stripped out (Table 1). Total resource exports dominate overall value-added exports with a 20.9% share. Energy becomes our leading value-added export. Industrial goods follow closely, just behind machinery and equipment and ahead autos. The order of the last three sectors was unchanged, with forestry, at 11% and agriculture and consumer goods less than 10%.

However, this ranking changes radically when the import content of exports is stripped out (Table 1). Total resource exports dominate overall value-added exports with a 20.9% share. Energy becomes our leading value-added export. Industrial goods follow closely, just behind machinery and equipment and ahead autos. The order of the last three sectors was unchanged, with forestry, at 11% and agriculture and consumer goods less than 10%.

Figure 2

Energy moves to the forefront for value-added exports because it has the lowest import content (12%) of any sector. Within energy, the import share of crude oil and natural gas production is the lowest, followed by electricity. Apart from an initial investment in some machinery and equipment, there are few opportunities to use imported parts.

The production of oil from the tar sands is a good example. After a large up-front investment in clearing the land and building structures, the crude bitumen is moved, often by large earth removers and trucks, for processing at an upgrader, before being shipped by pipeline. Apart from some imports embedded in the upgrader, few imports are used.

Further downstream, petroleum refineries raise the average for energy with a 41% import content. This partly reflects imported machinery and equipment used in refineries. More importantly, the crude oil being processed is often imported, either because foreign sources are cheaper (especially on the East Coast) or they are grades that are easier to process for particular uses (such as gasoline versus aircraft or diesel oil)

Industrial goods move up to the third-largest export share at 18.6% due to a relatively low import content of 28%. Most metals and non-metallic minerals import less than 20% of their inputs. Fertilizers have an especially low import content of about 10%, reflecting large domestic supplies of potash. Non-metallic minerals also use relatively few imported inputs. The low value-added of goods such as cement and concrete outweigh the cost of transporting these heavy goods very far (even inter-provincial trade in these goods is limited). An exception is aluminum’s 40% import content, mostly raw bauxite to be processed with Canada’s relatively cheap electricity. Excluding aluminum, other non-ferrous metals use imports for only one-quarter of their inputs.

Machinery and equipment and autos fall from our first and second largest gross exports to second and fourth for value-added exports because they import such a large share of their inputs. Autos fell the most as over half of all auto inputs were imported in 2001, and nearly 70% were imports of vehicles or parts. This industry has long had the highest import content, having pioneered the use of imported parts dating back to the Auto Pact in the 1960s. Firms are concentrated in southern Ontario, giving them ready access to parts makers in the northeast US. The growth of transplants of overseas producers has reinforced the trend to use more imports. The import content of vehicle assemblies is much higher than for parts manufacturers (59% versus 38%).

Machinery and equipment saw a rapid increase in its use of imports during the 1990s. Indeed, much of its rising share of gross exports during the 1990s reflected this change in its production process, not increased value-added output in Canada. Almost all these industries have a large import content, ranging from over one-third for aerospace, appliances and farm machinery to nearly one-half for ICT equipment. Over two-thirds of all imports by this sector are machinery and equipment itself, presumably parts (even in capital-intensive sectors like forestry and mining, machinery and equipment accounts for less than one-third of all imports).

Figure 3

Forestry products, our largest export decades ago, have slid to fifth place with 10.9%. They have a very low import content of just 19%, reflecting the relatively simple and local nature of logging, wood and pulp and paper production. Forestry, like its cousins in agriculture and mining, uses imported machinery and equipment and mining products.

Agriculture contributes 9.3% of our value-added export earnings. It imports 22% of its inputs, led by chemicals (mostly fertilizer). Like energy, primary producers of grain, livestock and fish have the lowest import content. Food manufacturers use imports (especially processed food) for over one-quarter of all inputs. This reflects how the manufacturing process, even for food, allows firms to search out better or lower-priced alternative sources both in Canada and abroad. Fish, fruit, vegetables and sugar refiners have the highest import content, reflecting limitations on domestic supply. Dairy, meat and grain products are less reliant on imports.

Within consumer goods, clothing and textiles have a relatively high import content of nearly one-third of all inputs. Over one-half of these imports are textiles and clothing destined for further processing. These industries increasingly outsource production overseas to maintain their competitiveness in the face of rising third-world supply. Pharmaceuticals, a driving force in the growth of consumer goods exports, also have a relatively high import content of 32%.

Not all imported inputs are goods. Globalization allows most industries to use a significant amount of imported services in producing exports, especially finance and business services. The finance and business services industries themselves import nearly one-quarter of their inputs from firms abroad in the same industry. But even in most natural resource industries, imported financial and business services account for between 6% and 10% of all inputs, slightly more than autos and machinery and equipment despite the latters’ longer experience in outsourcing abroad.

Conclusion

Canada’s export base has shifted in recent years from manufactured goods such as autos and machinery and equipment back to its traditional natural resource products, notably energy. The low import content of the booming resource sector is one reason our trade surplus has hit record highs, despite the slowdown in overall export growth after 2000.

This shift means a growing part of our economy does not face the intense global competition felt by many manufacturers. This may assure that Canada maintains its market share of exports, but could also dull our appetite for productivity gains and innovation.

The last decade highlights two facets of how globalization affects our trade flows. The 1990s were dominated by the increased use of imports as inputs, especially in manufacturing. But recent years have seen this process stall, and even partly reversed. Now the growth of natural resource exports is the most revealing measure of our integration into the world economy.

The recent boom in commodity markets has returned the spotlight to Canada’s natural resources, most of which are exported. The importance of resources to our overall exports is often discussed, with a figure of 40% commonly cited.1 This share has risen to 50% of gross exports thanks to the commodity boom of the last two years. But subtracting out the higher import content of manufactured exports raises the share of resources to over 60%. This puts Canada in a unique class of major industrial nations, alongside nations such as Norway and Australia, where resource exports dominate. They are the polar opposite of Japan, which imports most of its resources and exports almost none.

These estimates are usually arrived at by calculating the share of agricultural, energy, forestry and industrial materials in gross exports. But this method does not account for the difference between gross and value-added exports. As noted in our previous studies2, firms shifted to using markedly more imports in their production process in the 1990s. This phenomenon was most pronounced for autos and machinery and equipment, which import nearly half their inputs. This reflects the greater use by manufacturers of standardized parts, often made just across the US border or sometimes overseas.

As a result, much of the growth of gross exports in the last decade reflected the increasing use of imported components, not higher value-added exports. Value-added exports, which include only inputs purchased in Canada, are the key determinant of domestic output and jobs.

Conversely, many of our leading resource products have a largely extractive production process that requires few imports apart from machinery and equipment.

The implication is clear: the importance of industries such as autos that make liberal use of imports is overstated by gross exports, while industries that import less actually have a larger role than gross exports suggest, notably natural resources. This paper looks at the true role of resources in value-added exports in Canada.

The main motivation behind the growing use of imports was the relentless drive by firms to search out the lowest possible cost for inputs. As well, the rise in the Canadian dollar in the early 1990s lowered the cost of imports, giving firms an added incentive to purchase abroad. But the steady drop in the dollar from 1997 to 2003 took away much of this latter incentive, and the use of imported inputs leveled off in recent years. The recent recovery may encourage firms to buy more imported inputs.

Sectoral share of exports

In terms of the share of gross exports, autos and machinery and equipment led with about 22% in 2004. Despite their recent surge, the four resource sectors followed, led by industrial goods3 (notably metal products) and energy at 19% and 17% respectively. Forestry and agricultural products were next at 9% and 7%. Together, these four resource sectors accounted for just under half of all exports. Consumer goods trail at 4%, although they have grown the fastest, doubling their share since 1989, led by pharmaceuticals.

Figure 1

Figure 2

Energy moves to the forefront for value-added exports because it has the lowest import content (12%) of any sector. Within energy, the import share of crude oil and natural gas production is the lowest, followed by electricity. Apart from an initial investment in some machinery and equipment, there are few opportunities to use imported parts.

The production of oil from the tar sands is a good example. After a large up-front investment in clearing the land and building structures, the crude bitumen is moved, often by large earth removers and trucks, for processing at an upgrader, before being shipped by pipeline. Apart from some imports embedded in the upgrader, few imports are used.

Further downstream, petroleum refineries raise the average for energy with a 41% import content. This partly reflects imported machinery and equipment used in refineries. More importantly, the crude oil being processed is often imported, either because foreign sources are cheaper (especially on the East Coast) or they are grades that are easier to process for particular uses (such as gasoline versus aircraft or diesel oil)

Industrial goods move up to the third-largest export share at 18.6% due to a relatively low import content of 28%. Most metals and non-metallic minerals import less than 20% of their inputs. Fertilizers have an especially low import content of about 10%, reflecting large domestic supplies of potash. Non-metallic minerals also use relatively few imported inputs. The low value-added of goods such as cement and concrete outweigh the cost of transporting these heavy goods very far (even inter-provincial trade in these goods is limited). An exception is aluminum’s 40% import content, mostly raw bauxite to be processed with Canada’s relatively cheap electricity. Excluding aluminum, other non-ferrous metals use imports for only one-quarter of their inputs.

Machinery and equipment and autos fall from our first and second largest gross exports to second and fourth for value-added exports because they import such a large share of their inputs. Autos fell the most as over half of all auto inputs were imported in 2001, and nearly 70% were imports of vehicles or parts. This industry has long had the highest import content, having pioneered the use of imported parts dating back to the Auto Pact in the 1960s. Firms are concentrated in southern Ontario, giving them ready access to parts makers in the northeast US. The growth of transplants of overseas producers has reinforced the trend to use more imports. The import content of vehicle assemblies is much higher than for parts manufacturers (59% versus 38%).

Machinery and equipment saw a rapid increase in its use of imports during the 1990s. Indeed, much of its rising share of gross exports during the 1990s reflected this change in its production process, not increased value-added output in Canada. Almost all these industries have a large import content, ranging from over one-third for aerospace, appliances and farm machinery to nearly one-half for ICT equipment. Over two-thirds of all imports by this sector are machinery and equipment itself, presumably parts (even in capital-intensive sectors like forestry and mining, machinery and equipment accounts for less than one-third of all imports).

Figure 3

Forestry products, our largest export decades ago, have slid to fifth place with 10.9%. They have a very low import content of just 19%, reflecting the relatively simple and local nature of logging, wood and pulp and paper production. Forestry, like its cousins in agriculture and mining, uses imported machinery and equipment and mining products.

Agriculture contributes 9.3% of our value-added export earnings. It imports 22% of its inputs, led by chemicals (mostly fertilizer). Like energy, primary producers of grain, livestock and fish have the lowest import content. Food manufacturers use imports (especially processed food) for over one-quarter of all inputs. This reflects how the manufacturing process, even for food, allows firms to search out better or lower-priced alternative sources both in Canada and abroad. Fish, fruit, vegetables and sugar refiners have the highest import content, reflecting limitations on domestic supply. Dairy, meat and grain products are less reliant on imports.

Within consumer goods, clothing and textiles have a relatively high import content of nearly one-third of all inputs. Over one-half of these imports are textiles and clothing destined for further processing. These industries increasingly outsource production overseas to maintain their competitiveness in the face of rising third-world supply. Pharmaceuticals, a driving force in the growth of consumer goods exports, also have a relatively high import content of 32%.

Not all imported inputs are goods. Globalization allows most industries to use a significant amount of imported services in producing exports, especially finance and business services. The finance and business services industries themselves import nearly one-quarter of their inputs from firms abroad in the same industry. But even in most natural resource industries, imported financial and business services account for between 6% and 10% of all inputs, slightly more than autos and machinery and equipment despite the latters’ longer experience in outsourcing abroad.

Conclusion

Canada’s export base has shifted in recent years from manufactured goods such as autos and machinery and equipment back to its traditional natural resource products, notably energy. The low import content of the booming resource sector is one reason our trade surplus has hit record highs, despite the slowdown in overall export growth after 2000.

This shift means a growing part of our economy does not face the intense global competition felt by many manufacturers. This may assure that Canada maintains its market share of exports, but could also dull our appetite for productivity gains and innovation.

The last decade highlights two facets of how globalization affects our trade flows. The 1990s were dominated by the increased use of imports as inputs, especially in manufacturing. But recent years have seen this process stall, and even partly reversed. Now the growth of natural resource exports is the most revealing measure of our integration into the world economy.

Broad-Based Tax Reductions for Canadians

Broad-Based Tax Reductions for Canadians

Highlights

This Economic Statement proposes broad-based tax relief for individuals, families and businesses of almost $60 billion over this and the next five fiscal years. Combined with previous relief provided by this Government, total tax relief over the same period is almost $190 billion.

To improve productivity, employment and prosperity in an uncertain world, a bold, new tax reduction initiative will reduce the general federal corporate income tax rate to 15 per cent by 2012 from its current rate of 22.1 per cent. The general corporate income tax rate will decline by 7.12 percentage points between 2007 and 2012-giving Canada the lowest overall tax rate on new business investment in the Group of Seven (G7) by 2011 and the lowest statutory tax rate in the G7 by 2012.

The Government is seeking the collaboration of the provinces and territories to reach a 25 per cent combined federal-provincial-territorial statutory corporate income tax rate, to make Canada a country of choice for investment.

To support small business, the reduction in the tax rate to 11% for small business, currently scheduled to be reduced in 2009, will be accelerated to January 1, 2008.

The goods and services tax (GST) will be reduced by a further 1 percentage point as of January 1, 2008, fulfilling the Government's commitment to reduce the GST to 5 per cent.

The GST credit for low- and modest-income Canadians will be maintained at its current level even though the GST rate is being reduced. Maintaining the credit, while reducing the GST rate to 5 per cent from 7 per cent, translates into more than $1.1 billion in benefits annually for low- and modest-income Canadians.

The lowest personal income tax rate will be reduced to 15 per cent from 15.5 per cent, effective January 1, 2007.

The amount that all Canadians can earn without paying federal income tax will be increased to $9,600 for 2007 and 2008, and to $10,100 for 2009.

Together, these two measures will reduce personal income taxes for 2007 by more than $400 for a typical two-earner family of four earning $80,000, and by almost $225 for a single worker earning $40,000.

In order to make businesses even more competitive, it is essential that Employment Insurance rates be reduced for employers and employees. The Employment Insurance Chief Actuary's 2008 Report forecasts the break-even rate in 2008 will decline by 10 cents per $100 of insurable earnings for employers and 7 cents for employees.

Canada needs a tax system that rewards Canadians for realizing their full potential, improves standards of living, fuels growth in the economy and encourages investment in Canada. Actions already taken by the Government will reduce taxes on individuals, families and businesses by almost $130 billion over this and the next five fiscal years.

In total, this Economic Statement will provide almost $60 billion in additional tax relief over this and the next five fiscal years. Together, actions taken since 2006 will provide almost $190 billion over this period.

As the chart below highlights, about 73 per cent of the tax relief will have been provided to individuals and 27 per cent to businesses.

A New Era for Business Taxation in Canada

A New Era for Business Taxation in Canada

Canada needs an internationally competitive business tax system to ensure investment and economic growth, which will lead to new and better jobs and increased living standards for Canadians. Advantage Canada included a commitment to establish the lowest overall tax rate on new business investment (METR)[1] in the G7.

Chapter 1 notes the strength of Canada's economy, but also notes the risks and uncertainties we are facing. Chapter 2 points to our strong fiscal situation, illustrating that we have an opportunity few other countries have-to put in place measures that will bolster confidence and encourage investment at a time of economic uncertainty. This chapter sets out the measures the Government proposes to strengthen Canada's business tax advantage in the context of the potential downside risks to the economy.

The central element of these measures is a bold, new tax reduction initiative that will lower the general federal corporate income tax rate to 15 per cent by 2012. Broad-based business tax reductions support investment, job creation and growth in all sectors of the economy, including not only sectors with strong growth but also those facing greater challenges. Such tax reductions provide incentives for all businesses to succeed.

Broad-based tax reductions play a well-recognized role in improving productivity and economic growth, and in providing Canadians with more and better jobs and a higher standard of living.

Action to Date

The Government has already made significant progress towards making Canada's business tax environment more competitive through broad-based tax reductions:

The federal capital tax was eliminated in 2006.

The corporate surtax for all corporations will be eliminated in 2008.

The general corporate income tax rate is being reduced, from 21 per cent in 2007 (22.12 per cent including the corporate surtax) to 18.5 per cent by 2011.

The Government also established a financial incentive to encourage provinces to eliminate their capital taxes as soon as possible, and some provinces have acted to take advantage of this incentive. Since that initiative was introduced, Ontario and Quebec have legislated the elimination of their capital taxes by 2011, and Manitoba has announced plans to do so subject to budget balancing requirements.

Collectively, these actions will, by 2011, increase Canada's statutory corporate income tax rate advantage over the U.S. to 8.8 percentage points, and will allow Canada to achieve a meaningful METR advantage over the U.S. of 6.7 percentage points. Based on tax changes to date, by 2011, Canada's METR will fall to the second lowest in the G7 from the third highest.

Canada is close to achieving the Government's Advantage Canada target of the lowest METR in the G7. However, Canada's METR is still high relative to other Organisation for Economic Co-operation and Development (OECD) countries and small developed countries, and varies substantially by province. It is important in today's globally competitive marketplace that Canada strengthen its business tax advantage not only vis-à-vis the U.S. but also relative to its other trading partners.

Other countries recognize that competitive business taxes are key to economic growth and improved living standards, and they have been reducing their tax rates. We can expect that many of the countries that Canada competes with for investment will continue reducing business taxes in the years to come. That is why it is crucial that we take the bold actions needed to ensure Canada's business tax competitiveness.

Reducing the General Federal Corporate

Income Tax Rate

To strengthen Canada's business tax advantage, the Government is putting forward a bold, new tax reduction initiative that will lower the general corporate income tax rate to 15 per cent by 2012, starting with a 1 percentage point rate reduction in 2008 beyond already-scheduled reductions, to bring the rate to 19.5 per cent in that year. With these reductions, the general federal corporate income tax rate will decline by 7.12 percentage points between 2007 and 2012, a decline of one-third, and Canada's corporate tax rate will be the lowest in the G7. In addition, we will achieve our goal of having the lowest METR in the G7 by 2011 and will have a substantial business tax advantage over the U.S.-a statutory tax rate advantage of 12.3 percentage points and a METR advantage of 9.1 percentage points in 2012.

It is estimated that the reduction in the general corporate income tax rate to 15 per cent will reduce government revenues by $14.1 billion over this and the next five fiscal years.

Highlights

This Economic Statement proposes broad-based tax relief for individuals, families and businesses of almost $60 billion over this and the next five fiscal years. Combined with previous relief provided by this Government, total tax relief over the same period is almost $190 billion.

To improve productivity, employment and prosperity in an uncertain world, a bold, new tax reduction initiative will reduce the general federal corporate income tax rate to 15 per cent by 2012 from its current rate of 22.1 per cent. The general corporate income tax rate will decline by 7.12 percentage points between 2007 and 2012-giving Canada the lowest overall tax rate on new business investment in the Group of Seven (G7) by 2011 and the lowest statutory tax rate in the G7 by 2012.

The Government is seeking the collaboration of the provinces and territories to reach a 25 per cent combined federal-provincial-territorial statutory corporate income tax rate, to make Canada a country of choice for investment.

To support small business, the reduction in the tax rate to 11% for small business, currently scheduled to be reduced in 2009, will be accelerated to January 1, 2008.

The goods and services tax (GST) will be reduced by a further 1 percentage point as of January 1, 2008, fulfilling the Government's commitment to reduce the GST to 5 per cent.

The GST credit for low- and modest-income Canadians will be maintained at its current level even though the GST rate is being reduced. Maintaining the credit, while reducing the GST rate to 5 per cent from 7 per cent, translates into more than $1.1 billion in benefits annually for low- and modest-income Canadians.

The lowest personal income tax rate will be reduced to 15 per cent from 15.5 per cent, effective January 1, 2007.

The amount that all Canadians can earn without paying federal income tax will be increased to $9,600 for 2007 and 2008, and to $10,100 for 2009.

Together, these two measures will reduce personal income taxes for 2007 by more than $400 for a typical two-earner family of four earning $80,000, and by almost $225 for a single worker earning $40,000.

In order to make businesses even more competitive, it is essential that Employment Insurance rates be reduced for employers and employees. The Employment Insurance Chief Actuary's 2008 Report forecasts the break-even rate in 2008 will decline by 10 cents per $100 of insurable earnings for employers and 7 cents for employees.

Canada needs a tax system that rewards Canadians for realizing their full potential, improves standards of living, fuels growth in the economy and encourages investment in Canada. Actions already taken by the Government will reduce taxes on individuals, families and businesses by almost $130 billion over this and the next five fiscal years.

In total, this Economic Statement will provide almost $60 billion in additional tax relief over this and the next five fiscal years. Together, actions taken since 2006 will provide almost $190 billion over this period.

As the chart below highlights, about 73 per cent of the tax relief will have been provided to individuals and 27 per cent to businesses.

Canada needs an internationally competitive business tax system to ensure investment and economic growth, which will lead to new and better jobs and increased living standards for Canadians. Advantage Canada included a commitment to establish the lowest overall tax rate on new business investment (METR)[1] in the G7.